Source metrics snapshot

Percent / $BTimeline

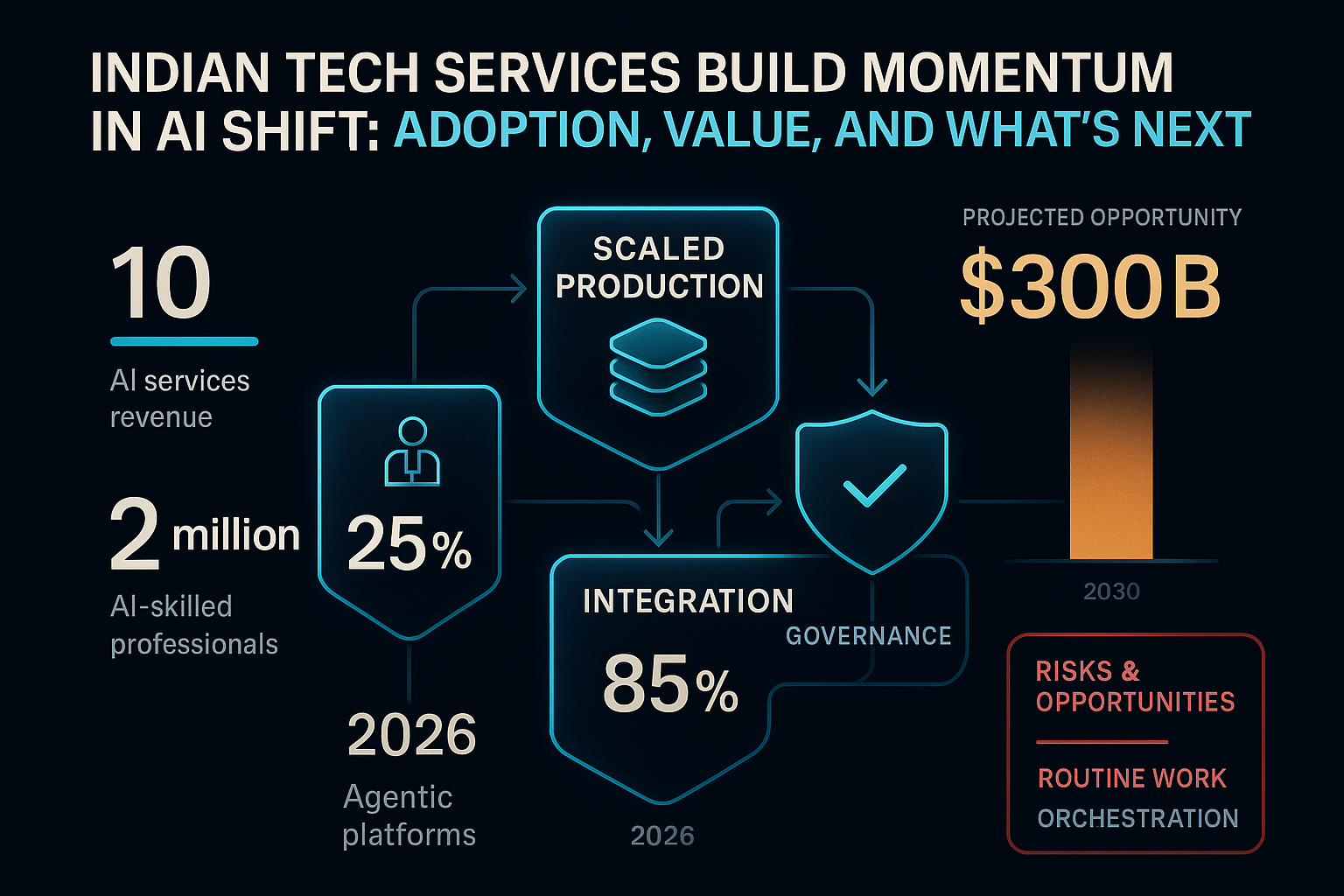

- 2026: AI production adoption reaches 25%

A quarter of sector firms move AI from experimentation to scaled production deployments.

- 2026: Agentic AI platform prevalence hits 85%

Vast majority of providers now have agentic AI capabilities available for clients.

- 2030: Sector opportunity targets $300–400B

Nasscom and industry leaders project total global AI services opportunity for Indian sector by 2030.

Context behind Timeline

AI’s impact on Indian IT services moved past the theory phase: it’s now measured by production deployments, workforce capability, and market traction. The transition affects delivery models, client expectations, partner requirements, and the competitive landscape both within and far beyond India.

Why it matters for Timeline

Operators and digital system builders can no longer treat AI as a testbed issue—enterprises now need integrated solutions that produce measurable results, demanding secure deployments, workflow redesign, and governance. Vendors who master this shift will shape new industry standards and secure a share of an enormous future market.

Key data behind the update

1 in 4 technology services firms has made the leap from experimentation to production deployments.

Annual AI services revenue is already $10–12B, signaling client demand for production-ready solutions.

Over 2 million professionals in India’s tech sector have AI skills (with 100–200K trained in advanced AI).

About 85% of tech service providers now offer agentic AI platforms.

Projected sector-wide opportunity in AI services is $300–400B by 2030, up to 30X current revenue.

Comparison criteria

Integrated AI platforms & production deployments

Higher complexity, platform focus, and value in orchestration2M+ AI-skilled; Rapid upskilling for advanced roles

Shift to specialist hiring and workforce retraining$10–12B AI services revenue; $300–400B projected by 2030

Explosive potential for firms who retool earlyProduction-ready, governed AI integration

Vendor value now in operational reliability & compliancePossible outcomes

High agentic platform adoption and production deployments

The sector transitions from automation provider to integrated enterprise transformation partner.Failure to build secure, unified data governance

Loss of trust or exclusion from high-value, regulated workflows; Opportunity moves to rivals.Signals to watch

Marks the real market opportunity and operationalizing of AI value, pushing standards and partnership expectations.

Growth rates here will determine which firms can capture high-value, orchestrated service work.

Enterprises are shifting from automation experiments to needing partners who ensure reliability and regulatory fit.

Signals both automation’s limits and the new premium on analytics, exception handling, and decision support.

Operators’ Guide: How Indian Tech Services Are Entering the AI Production Era

From Pilots to Production: What’s Shifted?

AI is no longer just an R&D showcase. With 25% of service providers deploying AI in production, new operating models are standardizing.

AI is being integrated into workflows, not merely automating isolated tasks. Providers now handle orchestration, security, and value delivery as core functions.

- Growing demand for end-to-end workflow redesign.

- AI platforms move from task-based tools to production stack components.

Workforce, Scale, and Market Opportunity

Over 2 million tech professionals now use AI; Advanced expertise (100–200K) is fast expanding. The sector is delivering $10–12B in yearly AI services revenue.

By 2030, the projected market for these services could grow more than 30-fold, provided providers excel at integration and specialist partnership.

- Mass upskilling is reshaping hiring and delivery.

- AI opportunity grows fastest in data, governance, orchestration, and modernisation.

The Next Competitive Vectors

Competition now centers on governance, security, and compliance—not just turn-key automation.

Clients will increasingly expect safe, integrated, and reliable AI operating models, putting pressure on vendors to build distinct domain expertise.

- Orchestrated operations win over simple automation.

- Vendor-client relationships shift to long-term partnership on risk and compliance.

Critical Upcoming Checkpoints

Key milestones include how broadly and deeply production deployments spread, how workforce capabilities scale, and whether Indian firms can deliver advanced, compliant models for regulated sectors.

Past fits of automation centered on labor reduction; This wave is about platform readiness and lasting value.

- Short-term: expansion in agentic platform usage.

- Medium-term: workforce upskilling and client production successes.