Why it matters for RPA market surge

For digital teams, the RPA surge is not just growth—it means redefining integration architecture, skills strategy, and vendor dependence as automation becomes enterprise-critical.

Operational consequences

- Acceleration in RPA adoption will stress digital team capacity to vet, integrate, and govern multi-vendor solutions.

- Enterprises may see hidden costs in upgrades, retraining, or responding to compliance breaches resulting from poor automation governance.

- Growth of the services segment signals a shift toward external dependency, increasing risk of supply chain disruption or knowledge gaps if partners change.

Evidence-backed metrics

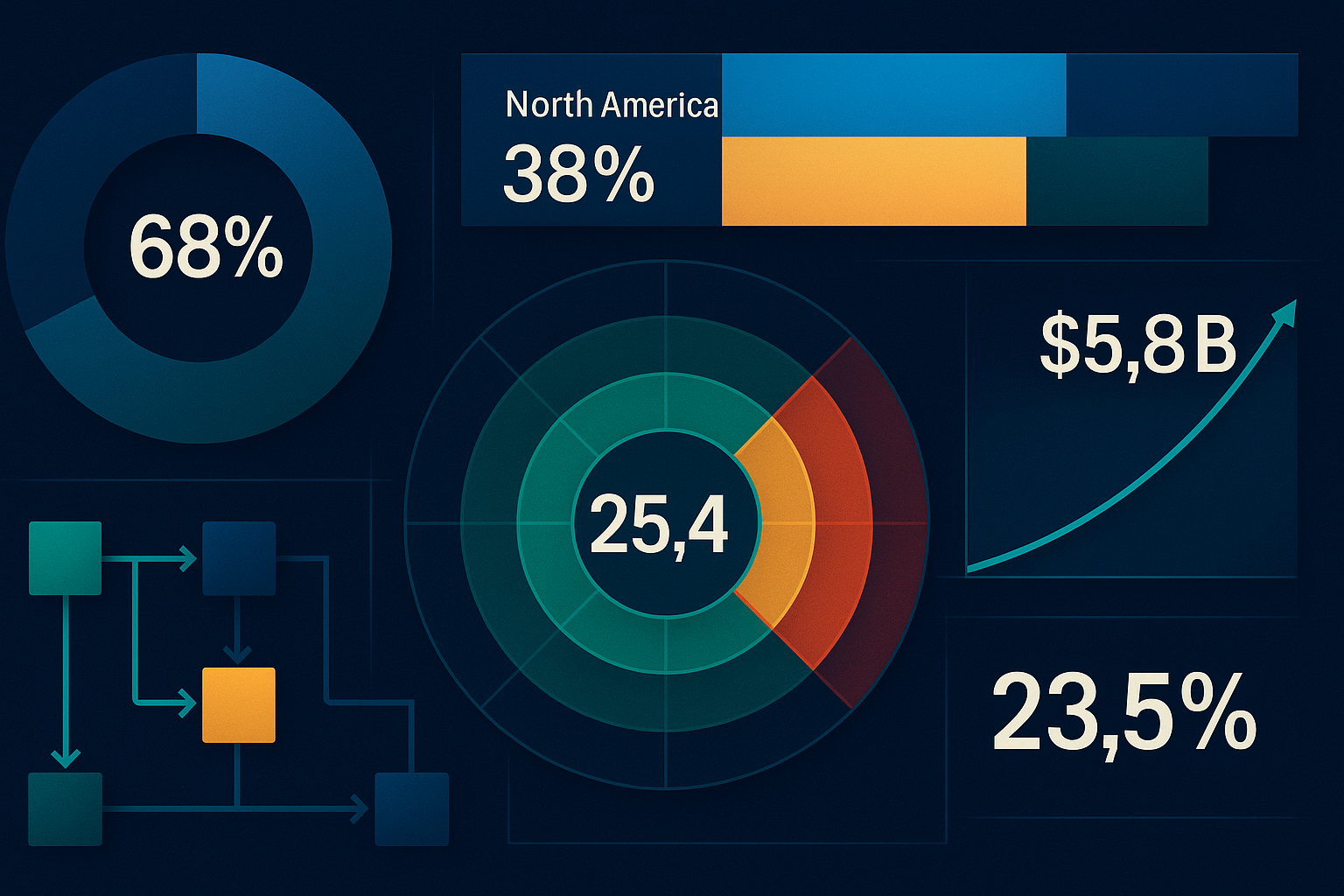

Indicates current scale and baseline for growth calculations.

Highlights the massive growth in addressable operational infrastructure for workflow automation.

Sustained high growth marks automation as a critical ops investment, not a niche tool.

Vast majority spent on core automation and orchestration platforms.

Indicates that benchmarks and best practices will likely be set in this region.

Shows distributed growth and regulatory exposure beyond the US market.

Numbers behind the shift

Source-reported valuesMarket context at a glance

Source-reported valuesNorth American market share

European market share

Reported CAGR

Decision criteria

AI/ML-powered RPA with cross-function orchestration

New skill requirements and architectural touchpoints needed.Dominance of platform and managed service providers

Switching costs and integration fragility increase.Human capital shifts to exception management and workflow design

Upskilling imperative; Risk of workforce disruption.Enterprise-wide compliance, process mining, oversight mandatory

Centralized governance and audit trail management required.Possible outcomes

Firms invest in process mining, change management, and cross-domain orchestration.

Achieve high ROI and resilience but require upskilling and active governance.Automation pushed through without proper oversight or upskilling.

Quick wins followed by higher rates of process breakdown and regulatory risk.Workflow impact

- Shifts staff focus from repetitive tasks to higher-value projects but may trigger workforce restructuring.

- Firms lacking strong change management and governance frameworks face higher failure and compliance risk.

- Vendor lock-in increases as software platforms command most investment; Services segment emergence may alter preferred sourcing models.

Signals to watch

Indicates maturing complexity and need for ongoing operational expertise.

Global architecture and playbooks must adapt to distributed regulatory and infrastructure demands.

Direct impact on architecture, requiring robust integration, not just cloud-first deployments.

RPA Acceleration Risks

Efficiency Upside and New Workflow Models

RPA platforms automate transactional and compliance-heavy workflows, releasing staff from repetitive chores to focus on exception handling and process design.

AI integration now handles unstructured data, recommendations, and advanced analytics—raising productivity and supporting quicker pivot for digital projects.

- Faster invoice, onboarding, compliance cycles.

- Process mining drives continuous improvement.

- Supports cross-functional and cross-system orchestration.

Integration and Governance Downsides

Dependence on leading vendors for software and managed services increases switching costs and exposes firms to integration or vendor stability risk.

As RPA becomes enterprise-wide, lack of centralized governance or insufficient upskilling exposes processes to error, non-compliance, or system failures. Regulatory complexity grows with multi-region rollouts.

- Vendor lock-in limits agility for future pivots.

- Process failures propagate quickly in integrated architectures.

- Compliance, audit, and upskilling costs rise as deployments scale.

Market Leadership and Strategic Shifts

North America will define early best practices; Europe’s regulatory landscape adds complexity. Service providers’ rapid growth shows a trend towards externalizing integration and support.

Teams operating in Asia Pacific will need to customize architectures and compliance playbooks, as the region outpaces others in growth rate but with less maturity in core standards.

- Monitor regulatory developments in EU and Asia.

- Prioritize vendor due diligence for global ops.

- Plan for multi-region compliance from the start.