Progress Software Key Financial Metrics Q2 2026

USD millions, margin as %Timeline

- Q2 2026 Earnings Release (June 30th)

Financial results surpass expectations across revenue, profit, and cash flow; Guidance raised.

- Data Platform Focus

Growth in products supporting AI-driven decisions highlighted by management as a performance driver.

- Innovation & Acquisitions Effort

Integration of recent acquisitions and technology investment ongoing to support future growth.

- Next Earnings, Q3 2026

Next checkpoint for confirming sustained ARR, margin, and customer retention trends.

Context behind Progress Software Q2 2026

Progress Software, operating multiple product lines for digital business and workflow automation, has established a pattern of emphasizing durable recurring revenue and customer retention. Management’s commentary positions data-driven infrastructure as a central pillar not just for operations but for the context AI needs to trigger actionable workflows. Compared to a year ago, their results reflect momentum in these themes, consistent with increased sector investment in workflow intelligence.

Why it matters for Progress Software Q2 2026

For business operators and workflow automation stakeholders, Progress Software’s Q2 2026 is a live test case for sustainable recurring revenue, high retention in B2B SaaS, and the increasing integration of data infrastructure with AI-powered workflow automation—a template influencing both vendor decisions and customer adoption standards.

Key data behind the update

A 7% YoY gain signals underlying customer demand and successful expansion.

2% annual constant-currency growth in ARR, reflecting stability and expansion.

Healthy 40% margin shows operational efficiency, even while investing in new areas.

Indicates the company retained all existing business and expanded some accounts.

Significant free cash flow supports further innovation or debt paydown.

Comparison criteria

7% increase (Q2 2026)

Progress Software is outpacing many platform peers.100%

Exceptional account stability and upsell discipline.40%

Higher profitability offers innovation investment headroom.2% (constant currency)

Signals still-expanding install base despite industry maturity.Possible outcomes

ARR increases above low single digits as AI-enabled workflows expand.

Progress Software cements a lead among stable B2B SaaS firms; Customers rely more on automation for core operations.Operating margin falls below 40% due to larger R&D or acquisition costs.

Stronger competition or rapid innovation cycles challenge cost discipline; Product pace accelerates but at earnings expense.Data platform usage for AI contexts slows; ARR stagnates.

Signal for potential market saturation or need for new feature sets; Platform diversification becomes critical.Signals to watch

Track whether the company can maintain or accelerate beyond 2% constant-currency ARR expansion.

Monitor launches or updates as these products underpin continued workflow automation growth.

Key to sustaining durable revenue and strategic advantage.

Impact future product synergy, margin, and growth trajectory.

Shifts in feature or pricing strategies may change industry dynamics.

Timeline and Context for Progress Software’s Q2 2026 Performance

Operational Signals: Connecting the Dots

Recent quarters showed Progress Software emphasizing multi-product stability and recurring revenue, now affirmed by Q2 2026’s figures.

Leadership’s repeated focus on data pipeline products for AI signals a strategic pivot toward infrastructure that enables intelligent automation.

- Recurring revenue reliability sustained amid a dynamic market.

- Data platforms central to new customer value in AI workflows.

- Continued innovation and acquisition integration observed.

Metrics That Set the Pace

Revenue, ARR, and cash metrics confirmed an upward trajectory, while extraordinary retention validates customer satisfaction.

Margin strength enables investment flexibility and enhances operating leverage, beneficial for workflow platform customers seeking vendor stability.

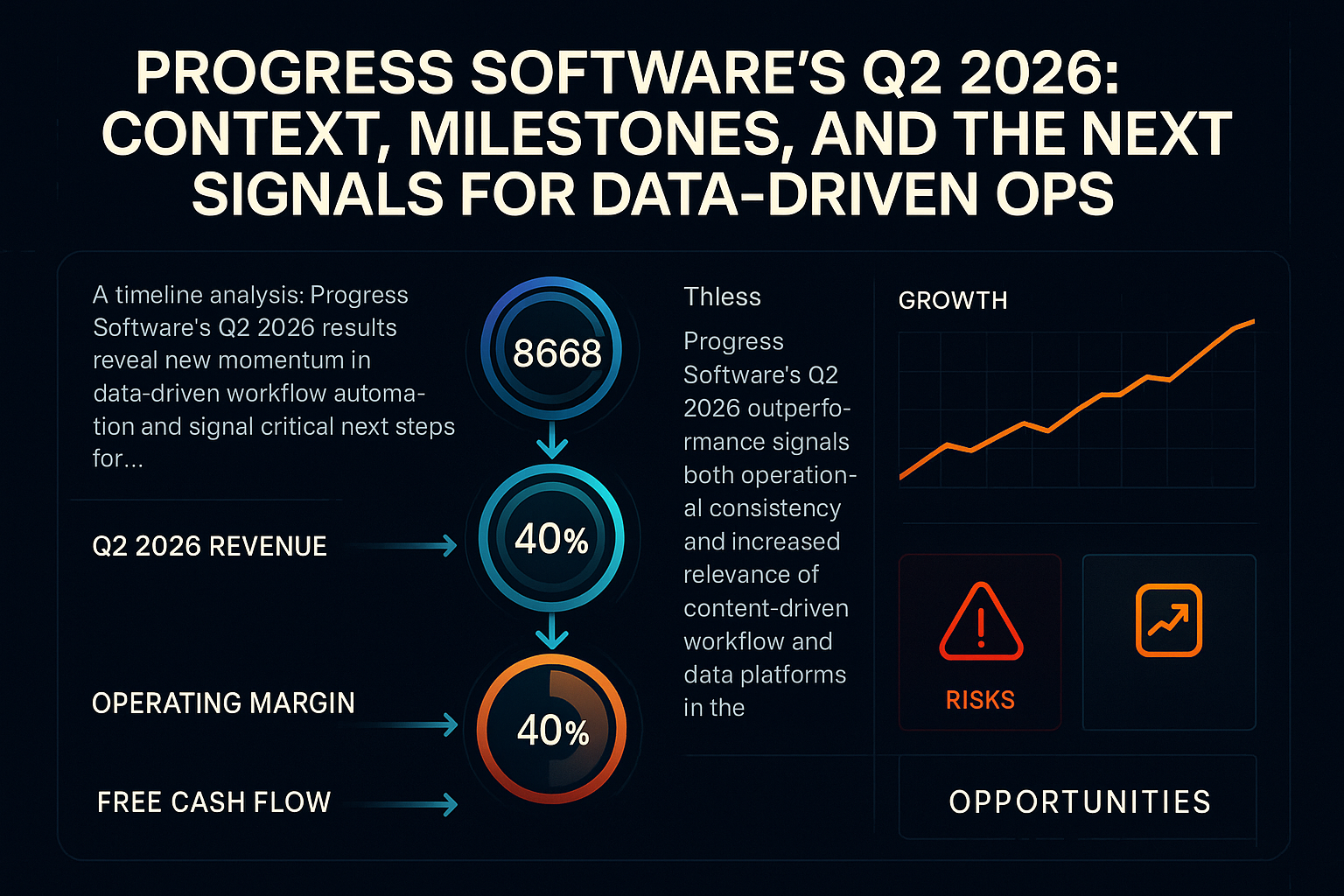

- Revenue: +7% YoY ($253M)

- ARR: $868M, +2% YoY

- Operating Margin: 40%

- Net retention: 100%, industry-high

Workflow Automation and AI Context

Expansion in content workflow solutions and data platforms is increasingly coupled to AI deployments, aligning Progress Software with digital system trends.

This integrated product approach anticipates rapid customer evolution toward automation based on contextual insights.

- Data-driven products powering AI-enabled decisions.

- Workflow solutions remain mission-critical.

- Vendor selection now favors integrated, resilient providers.

Next Milestones: Market and Product Signals

The company’s outlook and guidance hinge on sustaining innovation, high retention, and aligning offerings with AI adoption cycles.

Operators can track customer net expansion, margin discipline, product launches, and competitor responses as key signals.

- Monitor ARR trend for upward inflection.

- Watch for new workflow and data suite features.

- Track margin and retention consistency in future quarters.