Key data behind the update

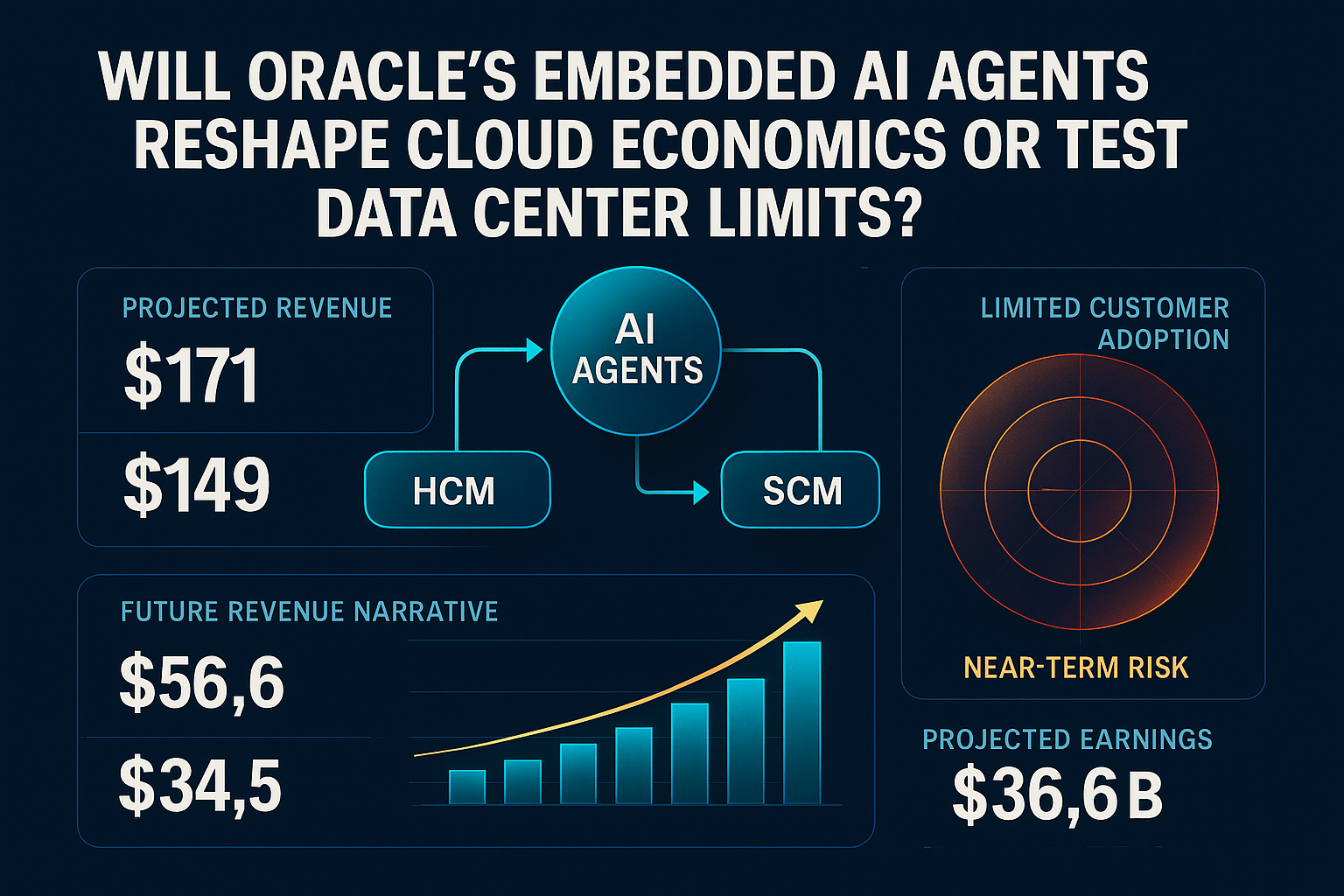

Oracle’s own narrative pegs future annual revenue at $171.1B by 2029, supporting a strong upside case.

A more cautious cohort expects $148.7B revenue by 2029, showing how adoption risk tempers the upside.

Oracle references a $638B backlog linked to its AI and cloud commitments, which must convert to lasting revenue.

Earnings could reach $36.6B by 2029 if Oracle’s integrated platform sees strong adoption.

Skeptical analysts see 2029 earnings at $34.5B, undermining a rapid payoff from AI agent investments.

Why it matters for Oracle AI Agents

For decision-makers building on cloud platforms, Oracle’s move signals a potential shift—if embedded AI agents deliver substantial workflow value and reinforce usage loyalty, it could make application-layer integration—not just raw infrastructure—the new competitive standard. If not, it highlights the risk of costly infrastructure strategies untied to day-to-day business results.

Context behind Oracle AI Agents

Oracle’s investment in AI agents attempts to move beyond infrastructure commoditization by embedding intelligence into the operational core of enterprise processes. This deepening of AI integration is meant to justify, and generate demand for, the company’s considerable ongoing data center and cloud buildout. The market’s reaction—especially in terms of real-world adoption and sustained revenue—will test if Oracle’s approach can outmaneuver both price-based competition and margin erosion.

Workflow impact

- May alter enterprise technology buying habits toward integrated workflow-AI offerings.

- Raises the stakes for cloud providers balancing CapEx intensity and applications stickiness.

- Challenges rivals to respond with their own embedded AI tools or risk losing inertia in workflow automation.

- Could influence valuation models for large SaaS/cloud firms depending on end-user adoption metrics.

- Highlights potential new customer concentration and debt risks if mass rollout does not occur.

Comparison criteria

Integrated AI agents in day-to-day workflows

Potential for higher stickiness and application revenue if adoption is strong.High CapEx, tied to backlog and customer follow-through

Magnifies the pain if contracts falter; Exposes leverage if proven.Dependency on immediate, large-scale workflow integration

Raises stakes; Either accelerates returns or increases financial risk.Timeline

- Late June 2026: Oracle unveils AI agent suite

Oracle publicly launches Manager Edge in Fusion Cloud HCM and Agentic Applications in Cloud SCM, embedding AI into enterprise workflows.

- 2026–2029: Market monitors workflow adoption and revenue impact

Oracle’s backlog, application revenue growth, and earning power are scrutinized by analysts amid competitive shifts.

Signals to watch

Early reference customers will provide evidence for or against the value proposition.

Changes in financial forecasts may indicate either validation or skepticism of the new strategy.

Rising customer dependence or churn will show if the playbook is driving sticky, diverse contract flows.

A robust response might erode Oracle’s first-mover advantage or catalyze a broader market pivot.

Oracle’s Embedded AI Agents: Market Shift or Strategic Risk?

AI Agents Move the Value Battleground

Oracle’s embedding of AI agents into HCM and SCM is designed to capture day-to-day workflow dependencies, not just sell cloud capacity.

This strategic repositioning targets pain points in leadership, planning, and readiness—areas essential for operational resilience.

- Agents serve as workflow glue for critical business processes.

- Oracle bets that stickiness at this layer will justify its massive CapEx.

Financial Projections Rely on Adoption, Not Just Announcements

Oracle’s 2029 revenue forecasts differ by over $20B between bullish and cautious scenarios, highlighting reliance on adoption.

Without strong customer uptake, even a record backlog risks being converted into low-margin or nonrecurring revenue.

- Analyst skepticism remains despite headline contract values.

- Earned revenue—not just contracted backlog—is the critical metric to watch.

CapEx Risk: Double-Edged for Shareholders and Customers

The company’s infrastructure buildout enables AI at scale but also exposes profitability if uptake lags.

Customer concentration is a rising concern if a few major cloud clients drive outcomes.

- Debt and capital risk increase with market uncertainty.

- Diversified application usage can mitigate exposure.

Competitive and Market Dynamics in Play

Rival providers could accelerate similar AI integrations, intensifying the workflow automation race.

If Oracle’s model succeeds, it could press others to innovate on workflow-centric AI, not just platform breadth.

- Operators should watch for fast-following competitors.

- Interoperability, not just feature parity, may decide the next cloud leaders.