Why it matters for BPO Surge

Enterprise operators face a two-sided challenge: unlocking intelligent automation via BPO partnerships and platform integration, while managing exposure to complex supply chains, data governance standards, and potentially brittle vendor ecosystems. Decision-makers must balance speed and flexibility with oversight and resilience.

Operational consequences

- System owners may face platform sprawl as BPO providers differentiate with proprietary tech.

- Exposure to service provider disruption, compliance liabilities, and data sovereignty increases with broader outsourcing.

- Procurement processes need to prioritize resilience, interoperability, and exit strategies as the BPO stack becomes integral to operations.

- Financial workflows become more efficient but potentially more opaque and harder to audit if heavily outsourced.

- Customer experience advances may outpace existing in-house capabilities, raising expectations and competitive pressure.

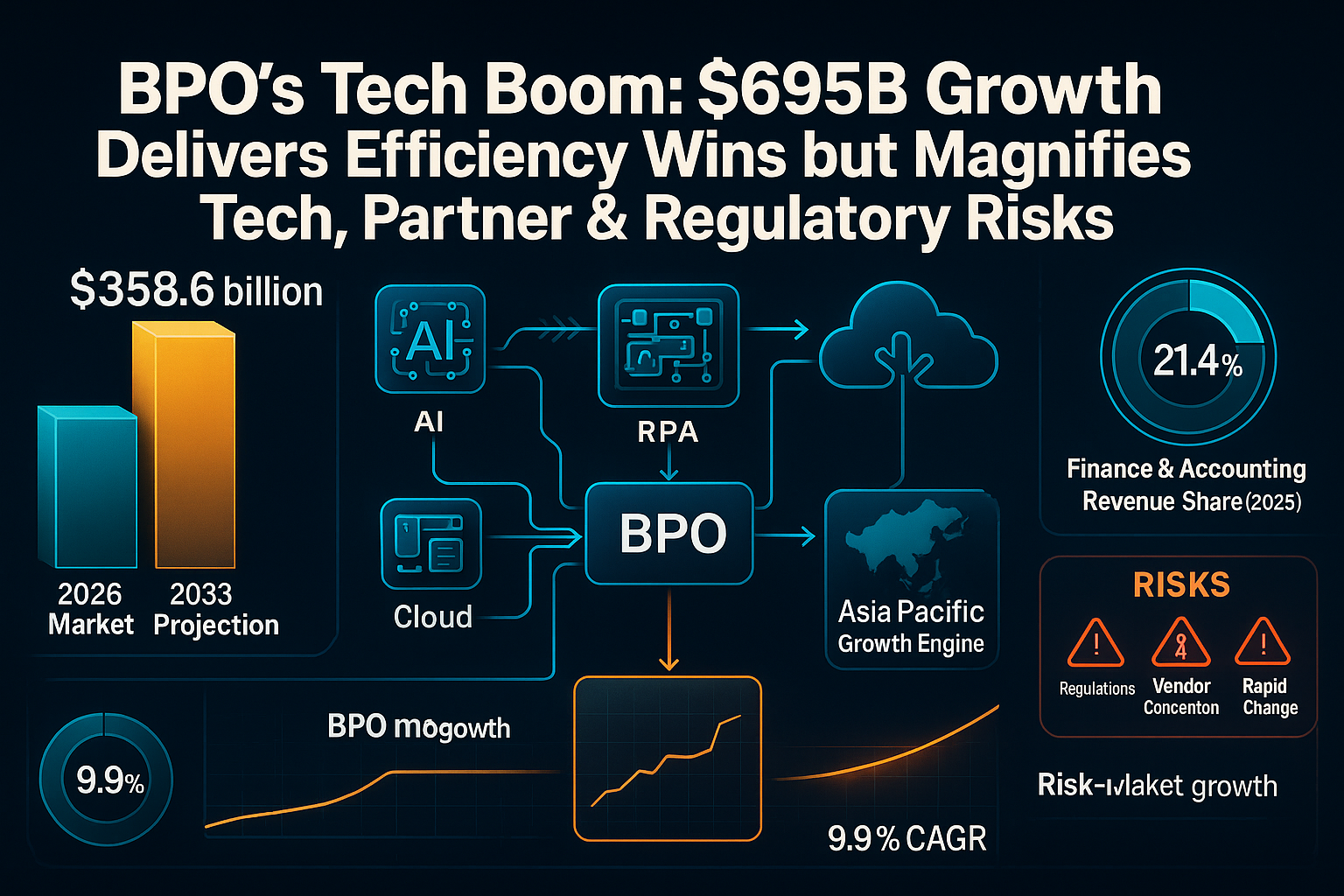

Key data behind the update

Represents near-term benchmark for market scale before majority AI/cloud penetration.

Forecasted doubling driven by tech-enabled workflow adoption and sector diversification.

Outpaces many traditional IT segments, signaling transformation urgency.

Finance and accounting outsourcing is leading revenue; Regulatory and transparency needs drive this trend.

Comparison criteria

AI-driven, cloud-first, integrated analytics.

Accelerates deployment, but reliability and integration complexity rise.Higher: compliance, vendor lock-in, partner dependency.

Resilience strategies become critical.Strategic: business innovation, transformation.

Shifts skillsets and vendor selection priorities.Asia Pacific as a key engine.

Procurement strategy adapts to APAC capabilities and cost-quality equation.Possible outcomes

Continued adoption of AI, RPA, and analytics in BPO processes.

Faster automation, shorter deployment cycles, but increased dependency on rapidly evolving tech.BFSI, healthcare and government clients require stricter data and process controls.

Limits some offshoring; Increases compliance and oversight costs for operators.Onshore BPO accounts for largest revenue in compliance-heavy fields.

Potential for shifting procurement away from pure cost to risk-aligned partner selection.Workflow impact

- Platform providers targeting BPO workflows can expand offerings in AI-enabled automation and omnichannel CX.

- Operators gain access to advanced analytics, but become more reliant on partner technology stacks and expertise.

- Onshore and offshore strategies shift in importance based on compliance risk, language, and operational alignment.

- Retail’s digital transformation accelerates amid rising demand for data-driven CX outsourcing.

- Asia Pacific’s role as a talent and infrastructure hub intensifies competition and option complexity for procurement teams.

Signals to watch

Indicates providers racing to differentiate on CX and data capabilities, not just cost.

Aims to expand portfolio and embed more digital ops tech in core BPO services.

Signals possible new competitive dynamics and emerging digital talent pools.

Confirms faster go-to-market for digital offerings and increased operational agility.

Where BPO’s Tech-Driven Growth Will Disrupt and Enable Operators

AI-Enabled Efficiency: Automation Accelerates, Reliance Intensifies

New integration of AI, machine learning, and RPA is rapidly reshaping how business functions are outsourced.

Automation is not just about cost—workflow orchestration and real-time insights now drive value as well as dependency.

- AI and workflow automation platforms reduce manual tasks, boosting speed.

- Predictive analytics and omnichannel CX upgrades become standard in competitive outsourcing bids.

Risk Frontiers: Vendor Lock-in, Compliance, and Audit Trail Challenges

Expansion of multi-functional outsourcing increases reliance on external partners for security, compliance, and resilience.

Onshore BPO’s lead in regulated sectors reflects ongoing scrutiny, but vendor consolidation raises single-point-of-failure stakes.

- Compliance-heavy sectors require stringent controls, limiting offshore gains.

- Systemic disruptions or tech failures can ripple quickly across dependent digital workflows.

Financial Ops and Retail: Case Studies in Opportunity and Exposure

Accounting and finance remain chief beneficiaries of BPO, prompted by growing needs for transparency and risk management.

Retail shifts to outsourced digital ops for personalized CX, data analytics, and coordination—but inherits tech and supplier risks.

- F&A leads segment growth but faces audit and governance risks with high externalization.

- Retail’s pace of digital adoption fuels both transformation and system integration complexity.

Platform Providers and APAC: Market Share, Talent, and Technology Mix

APAC’s ascendancy brings bigger talent pools, infrastructure spend, and innovation, but multiplies integration and supplier risks.

Providers investing in cloud, cybersecurity, and analytics differentiate on capability—not just price.

- Platform consolidation, M&A growth, and APAC expansion create new sourcing options.

- Cloud-first, distributed workforces become the new operating baseline.