AI Power User Penetration vs. Deal Size in Lower Middle Market

AI Power User Penetration (%)

Max Deal Size ($M)

Workflow impact

- Margin expansion possible for early adopters via streamlined workflows.

- Service enhancements differentiate smaller firms against larger, better-capitalized rivals.

- Automation becomes a baseline expectation ('table stakes') among high-growth platforms.

- Private equity partners value operational upgrades as much as financial capital.

- Competitive gaps will widen quickly as AI adoption accelerates.

Key data behind the update

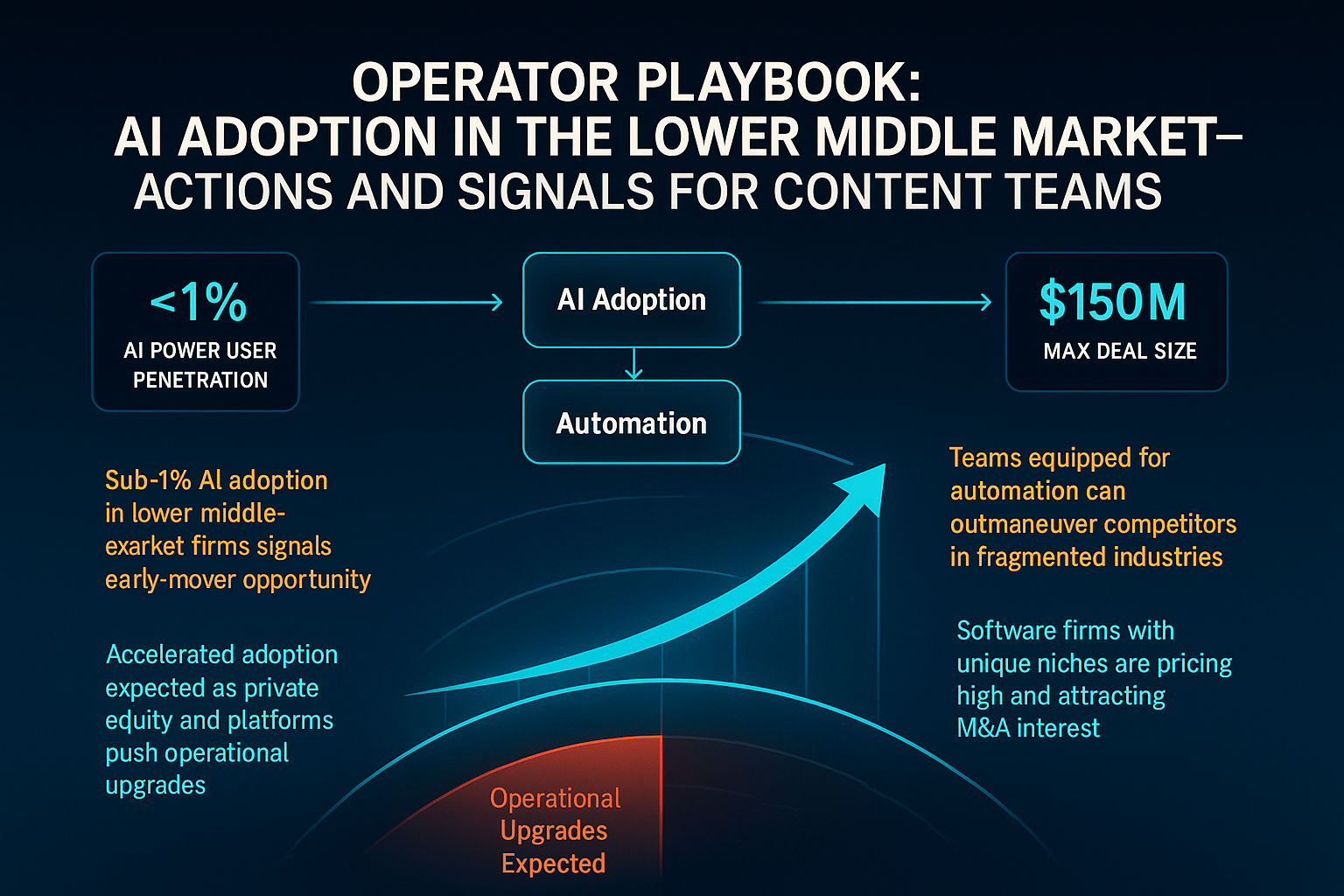

Less than one percent of such businesses are considered AI 'power users,' marking a significant early adopter gap.

Griffin's Wharf targets companies valued below $150 million, contextualizing the market's operational scale.

Operational consequences

- Early movers in workflow automation will capture outsized market share.

- Non-adopters risk diminished relevance and lower valuations during acquisitions.

- Operators must prioritize skill development in AI and automation to stay viable.

- Margin and growth benchmarks will reset higher as adoption accelerates.

Comparison criteria

<1% adoption among lower middle-market firms

Rapid acceleration forecast, brief window for early moversOperational enhancements now drive higher valuations

Tech-driven alpha is rewardedFragmented markets create pockets of inefficiency

Larger opportunity for tech-enabled platformsSignals to watch

Indicates normalization of automation as a baseline operation for growth.

Shows that buyers demand more than just financial returns—tech leverage now central.

Demonstrates practical business impact from early AI adoption.

Timeline

- Formation of Griffin's Wharf (2026)

New lower middle-market PE firm forms to pursue operationally enhanced deals.

- Current (2026): Sub-1% AI Adoption

Less than 1% of targeted firms are AI power users; Opportunity window is open.

- Next 5-10 Years

Forecast window for accelerated AI adoption and value creation in the segment.

Readiness Brief: Next Steps for Video and Content Ops Teams

Opportunity for Early Adopters

Teams who act now to integrate AI and automation tools into video and content operations can exploit the current early-mover advantage. Penetration is still under 1%, so process enhancements yield disproportionate gains.

Build multi-functional teams and relationships between IT and content ops, not just financial decision-makers.

- Survey existing workflows for automation gaps.

- Initiate pilot projects targeting routine content or metadata processing.

- Monitor peers’ adoption rates and partner with tech-forward service providers.

Competitive Risks and Consequences

Automation is now a baseline expectation. Platforms without digital and workflow upgrading will become less attractive in capital markets and M&A scenarios.

Being slow to adapt means becoming less differentiated—and likely less profitable.

- Assess team AI skills and upskilling needs now.

- Benchmark current workflow speed and accuracy against nearest competitors.

- Watch for sudden increases in peer feature rollouts or service quality.

Growth Strategy Alignment

Tech-driven differentiation, especially in fragmented verticals, will draw premium valuations and potential strategic bidders.

Smaller, nimble teams can use AI to punch above their weight, serving clients at larger-firm levels.

- Frame content innovation as an operational investment—not only an IT spend.

- Identify high ROI use cases: auto-tagging, distribution channel management, workflow error reduction.

- Engage top management in progress reviews and market scanning.