AI Workflow Adoption Snapshot

Workflow automation market (2025, USD B)

Workflow automation market (2031, USD B, forecast)

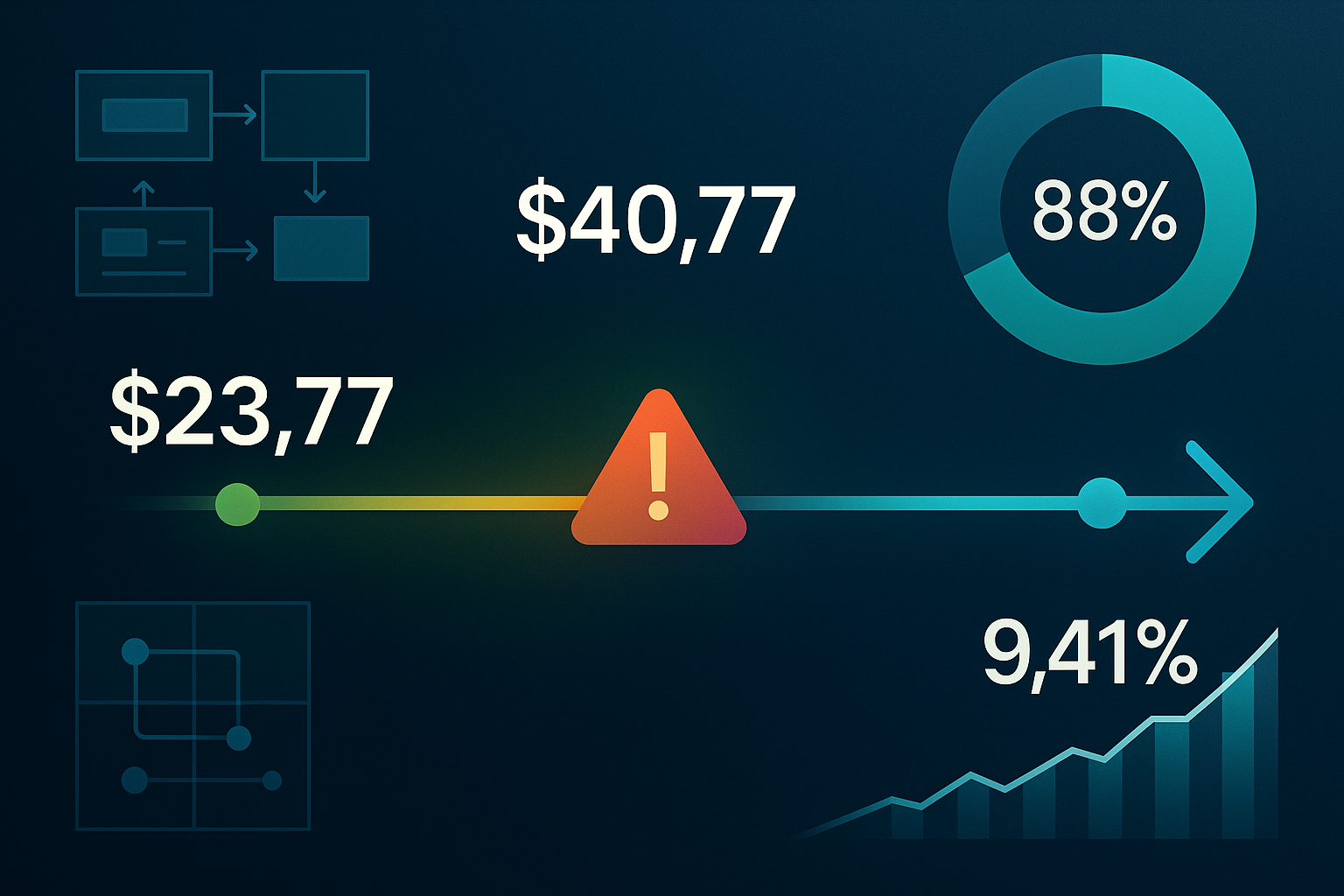

Hybrid IT environment share

Workflow impact

- Teams must reallocate skills: less traditional coding, more product analysis and ops engineering.

- Platform and governance layers require new investment as workloads and unreviewed software volume rise.

- Operational inconsistencies can expose organizations to risk unless robust application lifecycle controls are applied.

- Build-or-buy calculus changes: smaller teams can build more, but overall integration and maintenance risk grows.

- Failure to adapt operating models will erase efficiency gains from AI-driven coding.

Evidence-backed metrics

A recent OutSystems survey found approximately 66% of enterprises are using AI development tools for business applications.

The workflow automation sector was valued at $23.77B in 2025, with strong upward growth expected.

Market experts project the workflow automation segment will reach $40.77B by 2031.

The sector's compound annual growth rate is forecast at 9.41% over the coming five years.

Nearly 9 in 10 organizations now operate with mixed cloud and on-prem infrastructure, complicating workflow orchestration.

A majority of enterprises now run centralized automation teams that support hundreds or thousands of users.

Source data behind the story

Source-reported valuesOperational consequences

- Faster app delivery means more ongoing maintenance demand; IT and content workflows must increase capacity for integration and support.

- Siloed adoption of AI and automation tools can fragment the enterprise landscape, making unified monitoring and rollback more difficult.

- Operational headcount may shift from developer roles to platforms, governance, and lifecycle management.

Decision criteria

Product judgment and integration risk dominate

Organizations must invest in process design and ops, not just developer tooling.Varied code consistency; Requires stronger platform checks

AI-generated code increases risk of inconsistent, hard-to-audit deployments if unchecked.Two-thirds of enterprises use AI dev tools

Rapid mainstreaming increases pressure for supporting governance upgrades.Signals to watch

Monitor how leading vendors address consistency, review, and lifecycle issues as adoption spreads from prototypes to mission-critical systems.

Expect to see organizations hiring less for line-by-line coding, more for integration, platform discipline, and enterprise workflow support.

Track reported outages, inability to maintain code, or workflow fragmentation that exposes risks from under-governed AI outputs.

Timeline

- 2025

Workflow automation sector valued at $23.77B, as AI development reaches critical mass.

- 2026

AI-driven coding and workflow automation tools in use at two-thirds of large enterprises; Hybrid IT becomes dominant.

- 2031 (outlook)

Segment is forecast to reach $40.77B with continued double-digit growth; Operational and governance risks likely to determine value extraction.

AI Development Tools Transform Workflow Bottlenecks

Judgment and Operations Now Limit Digital Scaling

AI code generation platforms reduce time and resource barriers for building digital and content workflows, but the easy supply of new applications shifts the main constraint to organizational judgment. Knowing which projects to build and how they fit—not simply building them—is now the scarce skill.

- Coders less constrained, but platform engineers and business analysts become pivotal.

- Premature scaling can generate fragmented or unmaintainable digital estates.

Platform Guardrails and Operations Must Expand

Automation and AI tools create more endpoints and change the operational landscape. Without robust platform-level controls, review automation, and lifecycle management, organizations risk losing control of their application environments.

- Low-code offered uniformity; AI output may vary in structure and security.

- Centralized automation units support scaling, but few have unified, always-visible workflows.

Build-vs-Buy: More Power, New Risks

AI and low-code make in-house builds viable for smaller teams, but maintenance complexity and integration risk often climb faster than expected. The scrutiny should move to portfolio hygiene and the orchestration layer, not just the cost of app development.

- Buy vs build model tilts toward building—but with higher ongoing support demands.

- Vendors are racing to introduce improved integration and review features.

Hybrid IT and Unified Monitoring Required

Nearly all organizations now mix on-prem and cloud infrastructure. Visibility, orchestration, and unified monitoring are basic requirements, not aspirational goals. True platform-level automation remains rare despite increasing centralization.

- Most organizations have centralized teams but lack unified workflow oversight.

- Fragmented automation stacks hinder incident response and portfolio upgrades.