Why it matters for Agent Gateways

As AI agents multiply within enterprise systems, ungoverned access threatens production stability and cost management. Agent gateways promise central oversight but introduce new complexity, shifting organizational responsibilities and investment. Decisions now will determine whether these controls become standards and increase operational maturity—or introduce new pain points.

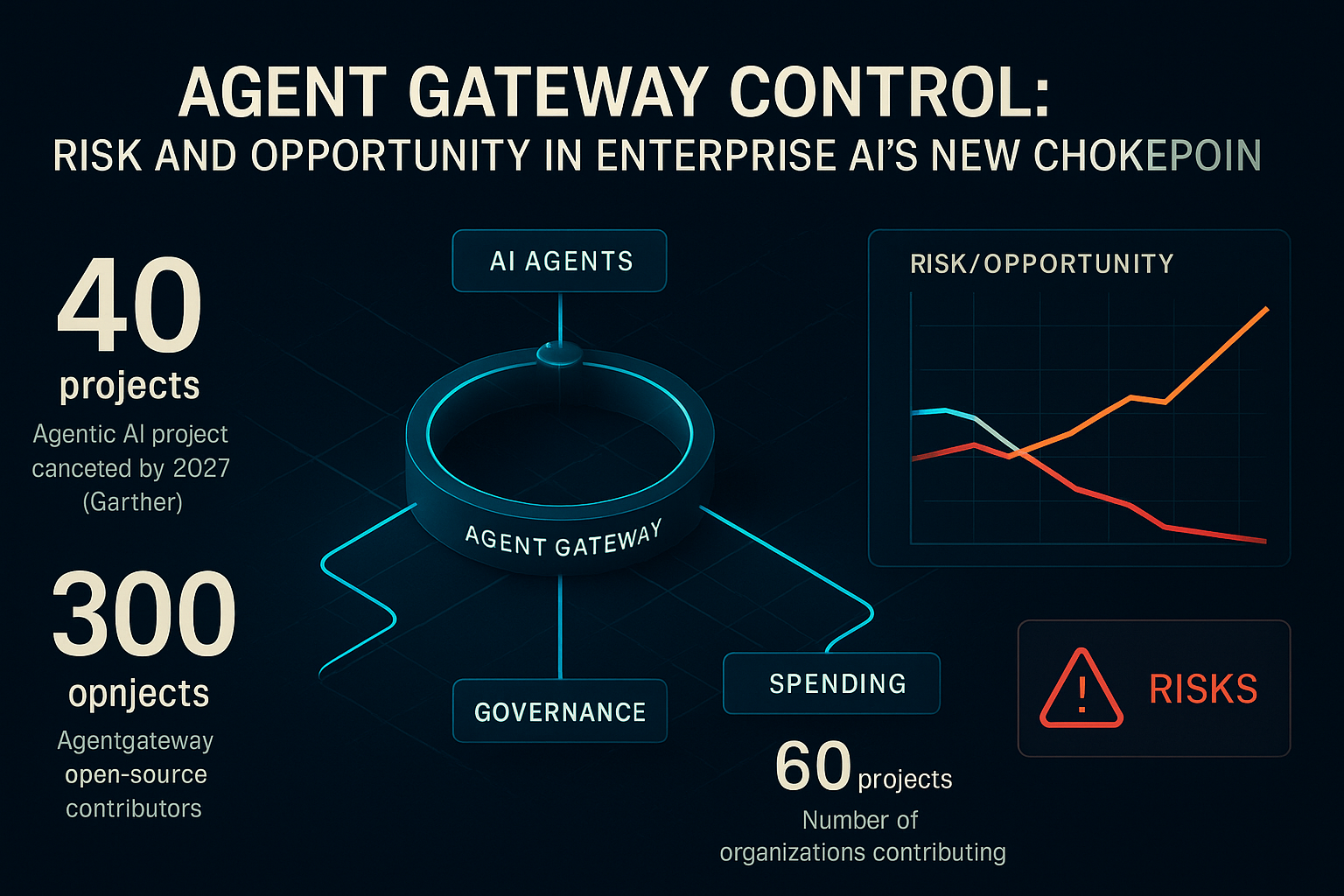

Operational consequences

- Organizations adopting agent gateways can rapidly enforce spending and permission controls, but risk creating new single points of failure.

- Fragmented enforcement or unclear ownership (proprietary vs. Open) can leave critical systems exposed if diligence lapses.

- Added operational costs and feature fragmentation could cause some projects to be canceled, echoing Gartner’s prediction of high agentic AI attrition by 2027.

Key data behind the update

A significant portion of projects are predicted to fail on cost or risk grounds, underscoring urgency of rigorous gateway evaluation.

Shows substantial collaborative momentum behind non-proprietary alternatives to commercial gateways.

Represents a cross-section of enterprise and software players, adding legitimacy to the open alternative.

Highlights agent gateways’ rapid elevation to core infrastructure status in open governance venues.

Comparison criteria

Agent gateway centralizes audit, token usage, and permissions.

Brings order and oversight but relies on the maturity of the gateway.Proprietary and open-source gateways now compete.

Choice between control, lock-in, and long-term extensibility.Gateways add a new line item, sometimes assuming rising agent volume.

Total cost and value may diverge if adoption plateaus or features lag.Gateways promise failover but face enforcement inconsistency.

Centralization can both increase resilience and raise systemic risk.Possible outcomes

Gateways become the standard for agent oversight across enterprises.

Centralized control reduces risk but could slow development or create vendor lock-in.High diversity or failure to deliver enforcement causes some projects—and the gateway market—to shrink.

Buyers may revert to custom or cloud-native controls, fragmenting oversight and auditing.Major players align with open-source governance or with locked-in suites.

Future procurement and integration decisions get influenced by alignment with broader industry standards.Workflow impact

- Enterprises gain auditability and cost visibility for agent activity across AI models and production tools.

- Security postures tighten as gateways allow for tool-level permissions and unified authentication—a key demand for regulated industries.

- Technology and procurement leaders must reassess ownership, cost, and enforcement details for both open-source and vendor-backed gateways, affecting platform choice and negotiation leverage.

- Vendors face pressure to expand from their original focus areas to cover new enterprise needs or risk being outpaced by open projects or large incumbents.

Signals to watch

Incident monitoring and compliance will drive broader scrutiny and product innovation.

Cloud-native solutions may absorb gateway capabilities, changing the market for specialized products.

Adopters must monitor production readiness and real security claims before standardizing on a solution.

Watching which independents survive and what is offered in security suites or open projects will define maturity.

Risk and Opportunity in Agent Gateway Adoption

The New Control Layer: Promise and Limitation

Centralized agent gateways claim to bring cost control, unified permissions, and observability for complex AI workflows. Quick oversight of agent activities now becomes feasible for operations and finance teams.

Yet, implementing gateways adds system complexity and operational expense, while real enforcement and interoperability remain uncertain due to fragmented market definitions.

- Enables granular permissioning and rate limiting for tool access.

- Offers per-agent and per-team spend attribution.

- Tech-preview limitations suggest governance is not fully mature.

- Size and scope of necessary coverage still debated by buyers.

Market Consolidation and Governance Divergence

Acquisitions and open-source pivots define the current landscape. Security vendors move to integrate gateways within broader platforms; Open foundations like the Linux Foundation attract cross-industry support.

For buyers, this forces choices between integrating with a dominant vendor suite for perceived security or embracing open governance at the cost of maturity.

- Palo Alto and Nutanix provide bundled proprietary options.

- Solo.io’s agentgateway offers a community-driven alternative.

- Gateways now marketed as infrastructure, auth, development, or security tools.

- Standardization remains unsettled, complicating procurement.

Cost, Enforcement, and the Path to Maturity

Gateways are positioned to help limit token and resource spend but can themselves be an additional cost center—especially if agent growth doesn’t justify scaling.

Incomplete enforcement and untested governance features, often in tech preview, raise questions about whether gateways will mature fast enough for production needs.

- Cost models may assume continued agent growth—creating risk.

- Inconsistent authentication/enforcement is a real failure risk.

- Audit trails improve but only if traffic routes through gateway.

- Gartner forecasts high attrition without clearer value and risk controls.